Variance Inflation Factor (VIF)

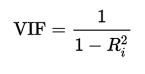

The Variance Inflation Factor (VIF) is a measure of colinearity among predictor variables within a multiple regression. It is calculated by taking an independent variable and regressing it against every other predictor in the model.

Including highly correlated variables in your model can lead to overfitting. If we overfit, then the model performs extraordinarily well on the training data but doesn’t generalize well when we try to use it on new data.

Small VIF values, VIF < 3, indicate low correlation among variables under ideal conditions. The default VIF cutoff value is 5; only variables with a VIF less than 5 will be included in the model. However, note that many sources say that a VIF of less than 10 is acceptable.